For multinational companies operating in China, a notable feature is the difficulty around repatriating cash. As it’s complicated and potentially costly for corporate treasurers to move cash offshore, having a treasury policy that accommodates the use of MMFs and understanding the domestic market for MMFs is all the more important. This is particularly important since MMFs run by domestic and international providers typically have very different risk profiles, with domestic providers being more return driven and retail centric.

MMFs comprised 37.3% of China’s mutual funds by AuM at the end of 2021, down from a high of 67% at the end of the first quarter of 2018. This reflects both an increased level of regulation, but also an increase in the overall size of the investment market, which authorities have been keen to support with preferential policies to encourage the development of the domestic mutual funds industry. This includes a tax exemption on dividends generated by funds, including MMFs.

The domestic MMF industry is predominantly made up of prime market funds, which are almost entirely senior debt funds and based on the constant net asset value model. There are six funds that operate as variable net asset value, but these represent less than 1% of the market.

Many of China’s MMFs have internet-based distribution models and China is well ahead of other markets in its use of mobile and online payment platforms such as AliPay and social media platforms like WeChat as distribution channels. This has made investing in MMFs easily accessible to retail investors where demand has been high, influencing the risk profiles of domestic funds to reflect the retail markets’ focus on return. The higher proportion of retail investors can result in volatility in flows in and out of the fund. Consequently, the size of a fund does not necessarily reflect the stability of a fund with one large fund losing 15% of its AuM in a single week due to the herd mentality often associated with retail investors.

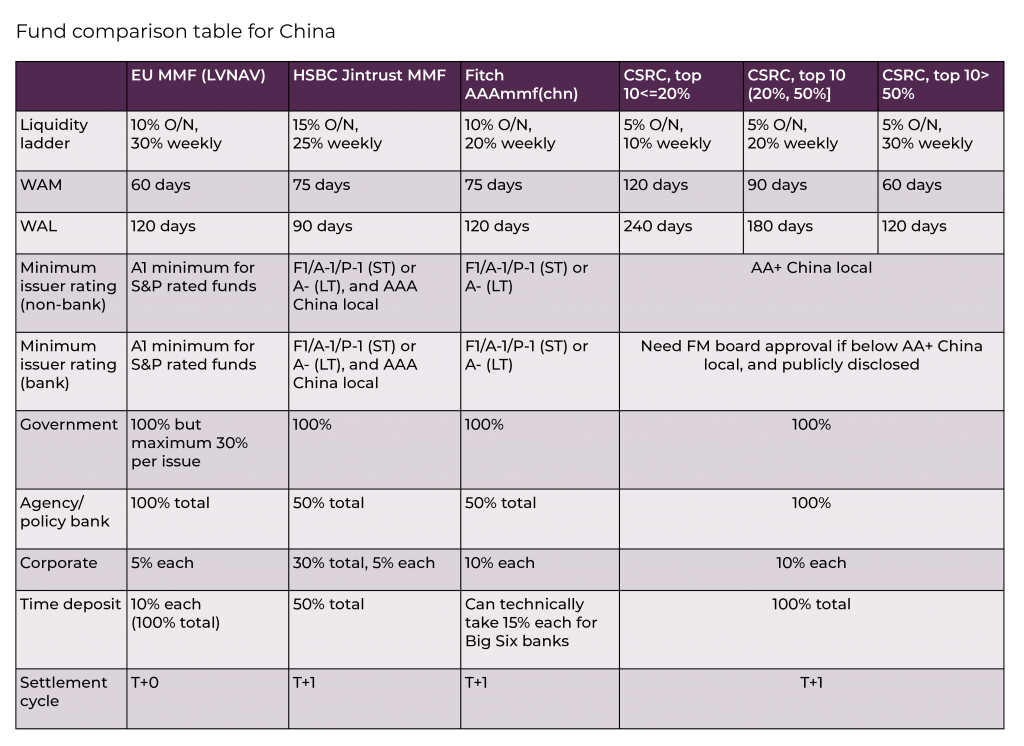

Diverging from international MMF norms, only a small proportion of China’s MMF industry is rated by a credit rating agency. Currently, Fitch is the only international rating agency to assign ratings to Chinese MMFs of which there are just three, with a combined AuM of ¥114bn as of April 2022. However, a MMF rating in China is unique and designed to specifically serve the needs of the domestic market, and the rating is denoted with a country-level suffix ‘AAAmmf (chn)’.

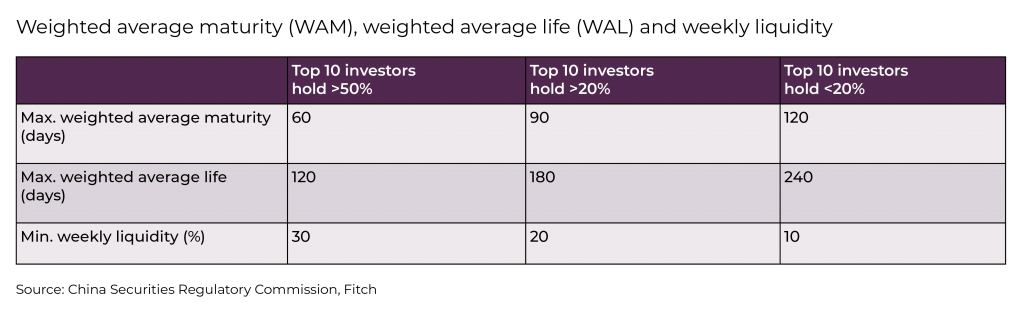

Corporate treasurers will need to be aware of variances between the rating criteria of Chinese MMFs and international alternatives they may be more familiar with. For example, while Fitch’s rating criteria limits Chinese MMFs to 75 days weighted average maturity (WAM) versus the regulatory maximum of 120 days, it remains higher than the maximum 60 days WAM by which international alternatives are constrained.

The market is quite concentrated with the top 10 fund managers accounting for some 47% of the industry by AuM at the end of 2021.

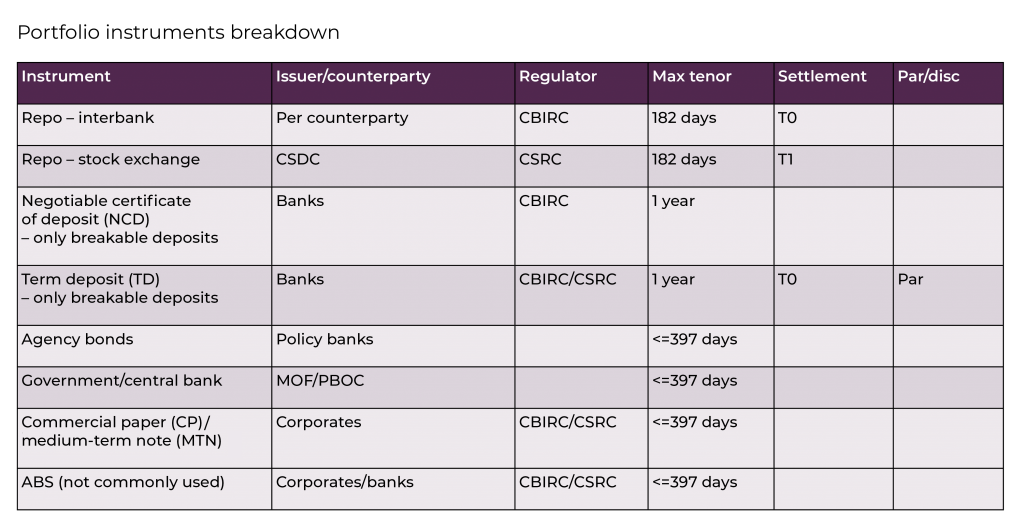

China has a broad market in terms of investment instruments. In addition to MMFs, there is a thriving interbank and exchange-traded repo market. There are also: agency bonds (which are policy bank bonds); central bank bonds; commercial paper issued by state-owned enterprises and by corporates; medium-term notes; time deposits; and standard certificates of deposit.